Steven Murphy / CHOICE GB / Earthism

UK Pensioners – The Wealthiest Generation In British History.

They Still Want More.

There is a conversation Britain is refusing to have.

Not because the evidence isn’t there. Not because the argument is weak. But because one group in this country has successfully made itself untouchable — politically, culturally, and morally — and nobody in power has the courage to say what the numbers have been saying for decades.

So let’s say it.

Britain’s pensioners — the generation now in their sixties, seventies, and eighties — have been the single greatest beneficiary of this country’s post-war expansion. They lived through the most extraordinary accumulation of wealth, assets, and state promises in British history. They took the benefits. And now, as the bill arrives, they are claiming it has nothing to do with them. That position is not just unfair. It is a lie the numbers expose every single time.

A 67 year old in 2026 was born in 1959. Over their lifetime almost every major economic indicator did not just rise — it multiplied. House prices rose from around £2,800 to nearly £300,000. A 67-fold increase. Not because this generation worked harder than any other. Because they owned assets during the greatest property boom in British history. Their homes became money-making machines that required nothing from them except ownership.

The stock market tells the same story. The FTSE 100 launched in 1984 at 1,000 points. It now sits above 10,000. A tenfold increase. Anyone who simply had savings, a pension, or investments saw their money multiply without doing anything exceptional at all.

The state pension rose from just over £2 a week in 1959 to £241.30 a week today. An increase of over 11,000%. Protected by the triple lock — a guarantee that exists for no other benefit in Britain — it became the most protected income in the country. No other group gets this. Just pensioners.

On top of that, real wages tripled between 1959 and 2008. Home ownership expanded from 42% to 71%. University was free. Energy was cheap. Jobs were secure. The tax burden was lower. The population was 52 million, not 68 million. Every single indicator moved upward. Everything expanded. Everything was affordable — or appeared to be.

And the national debt? It rose from £17 billion to nearly £3 trillion. A 170-fold increase.

That is not just a number. It’s a confession. It represents decades of the country spending more than it earned, consuming more than it produced, and borrowing from the future to pay for the present. Decade after decade, the gap between what Britain spent and what it raised in taxes was filled with borrowed money. And decade after decade, the generation that benefited most from that spending voted for governments that kept it going.

Before we go any further there is one fact that needs to be said out loud. Because the entire political story around pensioners depends on it never being said. The pensioner cohort currently demanding protection from any reform — currently claiming victimhood, currently arguing they cannot bear any changes to their entitlements — is the wealthiest retired generation in Britain’s history. Not by a little, by a distance that has no historical comparison.

The housing wealth alone makes the case. This generation bought homes at three to four times average earnings. Those homes are now worth twelve times average earnings. The total housing wealth held by over-65s in Britain exceeds £2.5 trillion. A huge proportion own their homes outright — no mortgage, no debt, pure equity that built up while they got on with their lives. Many own additional properties on top. That wealth was not the product of exceptional hard work or unusual sacrifice. It was delivered by demographics, cheap credit, restricted housing supply, and time. They were in the right place. They owned the right thing. The market did the rest.

Final salary pension schemes — which have been closed to virtually every worker under fifty — still pay out to millions in this generation. These schemes guarantee a retirement income that rises with inflation no matter what happens to the economy or to the workers currently paying for them. That level of security has been permanently removed from younger workers. The people drawing these pensions are drawing something that simply does not exist for those behind them.

And then there are financial assets. Decades of stock market growth have been captured mostly by older savers through pension funds and ISAs built up over the expansion years. That wealth has compounded over time and concentrated in the over-60s to a degree never seen before in this country.

The Office for National Statistics confirms it. Wealth in Britain is more concentrated in the over-65 age group than at any point ever recorded. The average combined wealth — housing, pension, and savings — of a household in their late sixties in Britain today exceeds £500,000.

That is the generation claiming it cannot absorb reform. That is the generation calling itself vulnerable. That is the generation whose politicians argue, with a straight face, that touching the pension would be an act of cruelty.

Half a million pounds of average wealth. And they are the victims.

Now look at the generation being asked to fund them. A 30 year old today has a fraction of the wealth that the same age group had thirty years ago. They are poorer at the start of their adult financial lives than any generation in living memory. Not because they work less hard. Not because they are less capable. But because the system that built the older generation’s wealth has been built on their backs.

The wealthiest retired generation in British history is being funded by the poorest-starting working generation in living memory. And the wealthiest generation is arguing the arrangement is not generous enough.

That needs to be said out loud. Without apology.

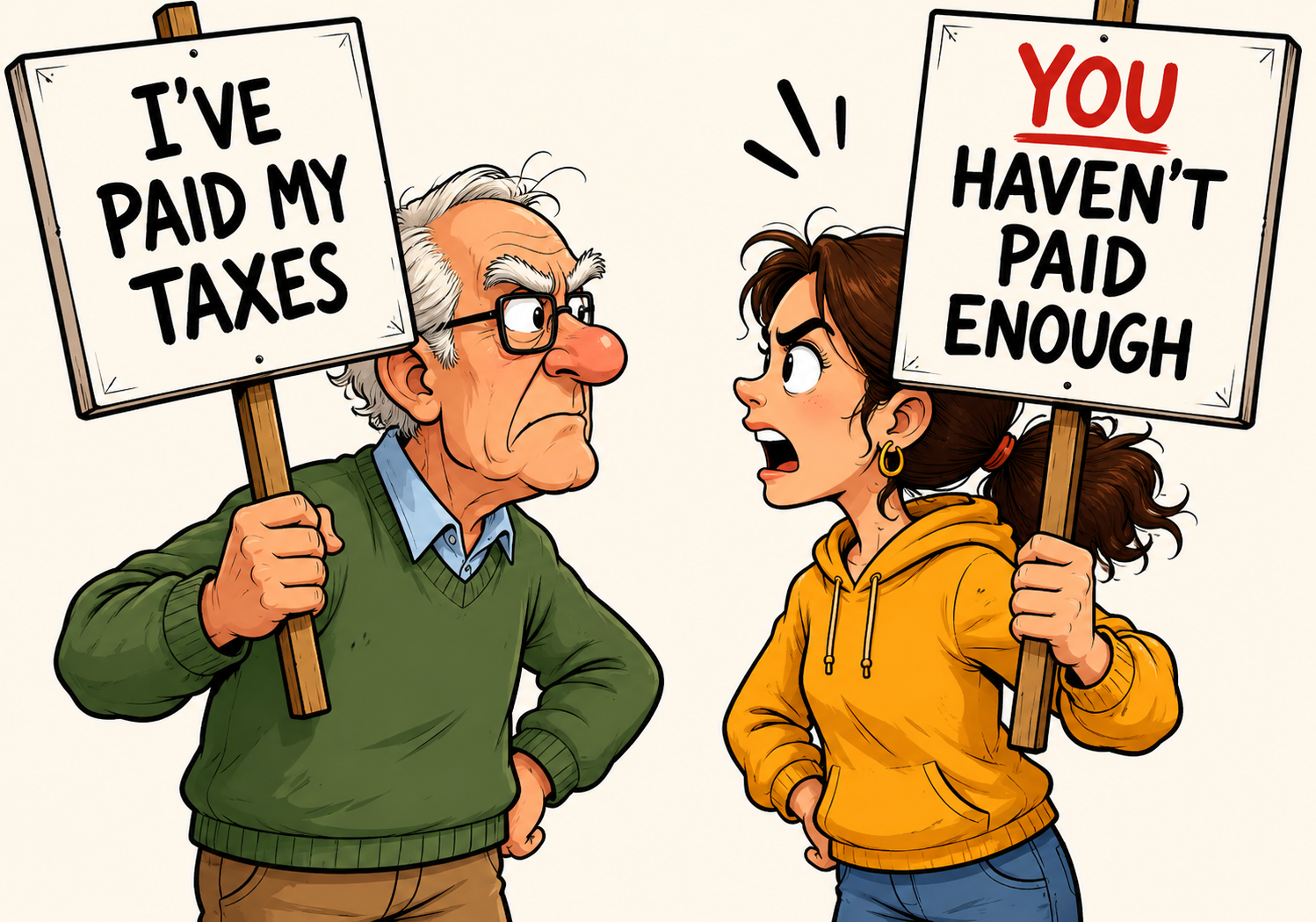

“I paid my taxes. I contributed. I am owed this”. This is the argument that comes up every single time pension reform is mentioned. It is the wrong argument, and we have the numbers to prove it.

The state pension is not a savings account. There is no savings pot or investment fund. There is no pile of money somewhere with your name on it built up from your contributions. The state pension is a pay-as-you-go system. Today’s worker’s pay for today’s pensioners. That is how it works. That is the reality. The “I paid in” argument is not just misleading. It is factually wrong.

But let’s take the spirit of it at face value. Let’s say the claim is simply that taxes were paid and the system was funded. Fine. Then the question is simple:

Was enough tax paid?

No. Demonstrably, provably, arithmetically no.

Britain has run a deficit in 21 of the last 23 years, and in most years since the 1970s. The national debt is now approaching £3 trillion — but that figure excludes the government’s two largest liabilities: around £1.4 trillion of unfunded public sector pensions and a further £5–6 trillion of State Pension obligations. Taken together, the UK’s true long‑term commitments are closer to £9–10 trillion.

The pension system is in structural deficit, and the state is making promises it cannot fund from current tax revenues. This is not opinion. It is the consistent assessment of the Office for Budget Responsibility, repeated in every long‑term fiscal forecast for more than a decade. If enough tax had been paid there would be no deficit. If contributions had matched the promises there would be no debt spiral. If the system had been properly funded the numbers would balance.

They don’t balance. They have never balanced. And the generation that paid their taxes paid them at rates set by governments they voted for — governments that deliberately kept taxes lower than the promises they were making. The debt and deficit is not an accident of history. It is the direct result of political choices made over fifty years by an electorate that is now retired. They paid their taxes, they just didn’t pay enough. The numbers say so. That is not a moral judgement, it is a mathematical fact.

So here is the crux of the matter, the pensioner cohort didn’t stumble into this situation. They didn’t inherit it by accident. They were adults — voting adults — for the entire period during which every one of these problems was created.

A person who is 70 years old today has been able to vote since 1974. They have voted in every general election during which the national debt doubled, trebled, and exploded beyond recognition. They were in the electorate when housing policy failed a generation. When pension reform was avoided, repeatedly. When infrastructure was left to decay. When government after government chose what felt good today over what was sustainable tomorrow. They had the opportunity to change trajectory, they chose not too.

And older voters do not just vote. They vote in massive numbers. Turnout among over-65s consistently exceeds 70%. Among 18 to 24 year olds it rarely gets above 50%. British politics gives its attention to the people who show up. That is not a conspiracy. It is democracy doing exactly what it is supposed to do — and being used, election after election, to protect one generation at the direct expense of the next.

The triple lock wasn’t forced on pensioners, it was given to them. By politicians who knew that the pensioner vote was the most reliable vote in the country. Winter fuel payments. Free TV licences. Protection from benefit caps. Every single one of these was a deliberate political choice, made possible by political power, used by a generation that showed up and voted for it every time.

At every point when the direction could have changed — when a different choice could have been made, when the long-term health of the country could have been prioritised over short-term comfort — this generation had the power to demand it. They chose not to. They chose what protected them. Every time. Across fifty years of elections. They knew what they were doing. They chose it. You do not get to choose for fifty years and then walk away from what your choices produced.

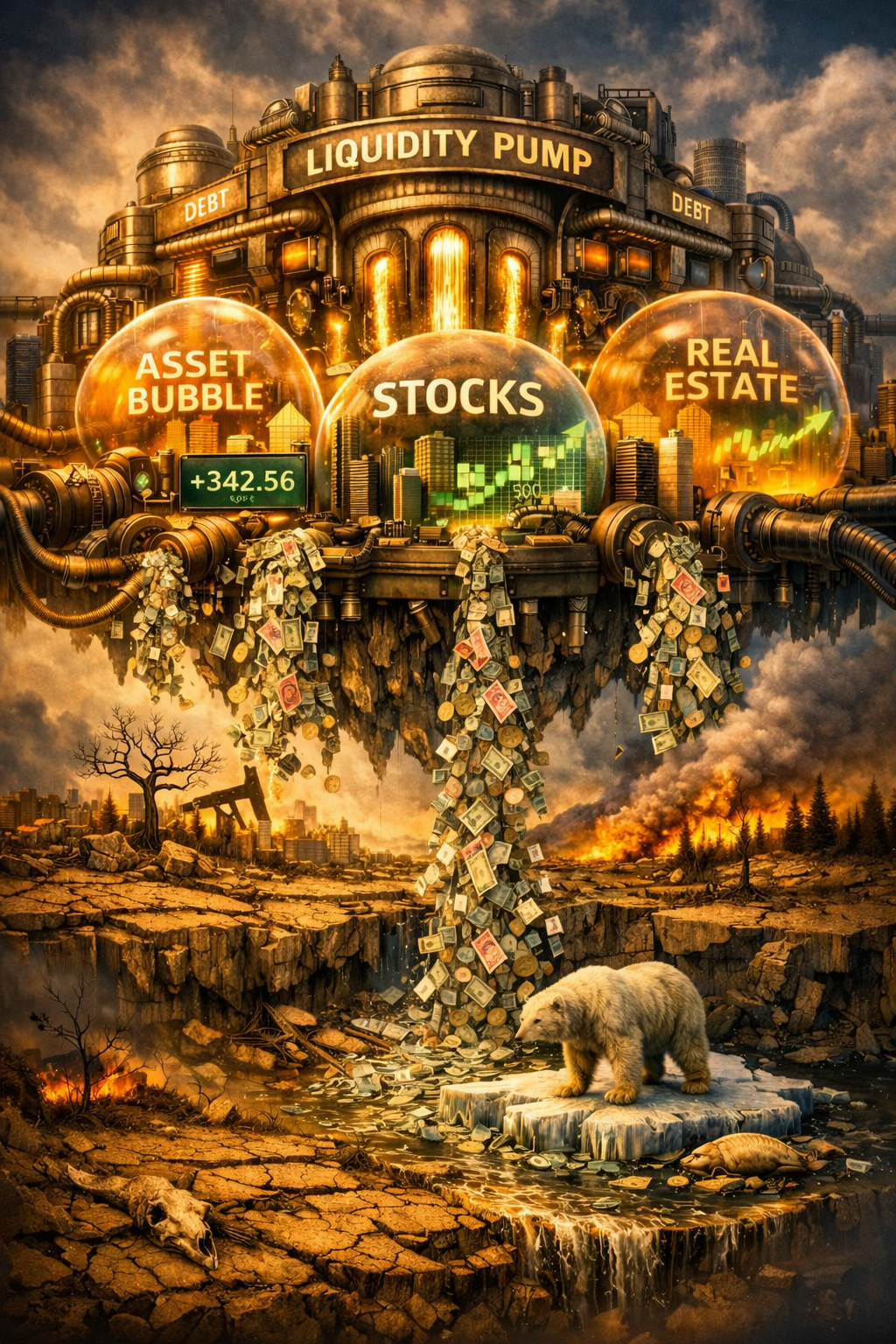

The 2008 financial crisis was the moment the bill should have arrived, a crash that should have changed everything. Banks had spent decades lending recklessly, borrowing irresponsibly, and selling debt they didn’t understand and couldn’t honour. But the banks were not alone. Society itself had spent decades living beyond its means — spending more than it earned, borrowing more than it could repay, and voting for governments that kept promising more than they could fund. The crash was not a bolt from the blue. It was the inevitable result of decades of collective recklessness. The system deserved to fail. The people who built it deserved to feel the consequences.

They didn’t. Governments and central banks around the world refused to let the reckoning happen. What followed was the biggest economic intervention in modern history. Interest rates were collapsed to near zero and kept there for over a decade. Hundreds of billions of pounds were printed through a policy called quantitative easing — money created from nothing. And in doing so, currencies around the world were deliberately devalued. The purchasing power of money was destroyed. The return on saving was wiped out. The real cost of debt was artificially crushed.

Three levers. Pulled simultaneously. In the same direction. Print money. Destroy interest rates. Devalue the currency. Each one on its own would have been extraordinary. Together they represented the complete surrender of economic reality to protect the existing order — and the people who owned it. And the consequences fell with absolute clarity on opposite sides of one dividing line. Do you own assets or don’t you?

If you owned assets — property, shares, savings portfolios — the printed money flowed straight into their value. Prices rose. Wealth grew. The rescue left you richer than the crash would have done.

If you owned nothing — if you were a younger worker trying to save for a deposit, trying to build some financial security, relying on your wages rather than your capital — the same policies worked against you from every angle at once. Your savings earned nothing. Your money bought less. The things you needed to buy kept getting more expensive. The debt you had to take on was artificially cheap, pushing prices even higher. You were effectively subsidising the wealth of the generation above you through the deliberate destruction of the conditions that might have let you catch up.

The pensioner cohort did not just survive 2008. They were rescued from it, rewarded by it, and came out of it richer. The money printing was the final and most powerful wave of the great inflation era that had already made them the wealthiest retired generation in British history. First wages inflated. Then property inflated. Then markets inflated. And when the moment came that should have brought a correction — when the recklessness should finally have been punished — governments printed money and inflated everything all over again.

The consequences were cancelled on their behalf. And the people who had no hand in creating the crisis, no power to stop the bailout, and no share in the gains that followed were left to pay for all of it.

That is not bad luck. That is not coincidence. That is a system doing exactly what the most powerful generation in British political history needed it to do.

While pensioners were protected from every economic shock of the last two decades the younger generation was not just left exposed. They were squeezed from every direction at once. And every single squeeze has a direct cause.

Start with housing. The older generation bought homes at three to four times average earnings. Today it is twelve times. A buyer purchasing a £300,000 home with a 10% deposit borrows £270,000. Over a 35 to 40 year mortgage the total repayment including interest approaches £550,000 to £600,000. They repay roughly double what they borrowed. They carry that debt for most of their working lives.

And who gets the money from that inflated sale? Frequently an older homeowner. Someone who bought at £30,000, did nothing while the market did the work, and is now sitting on equity worth ten times what they paid. The younger buyer’s debt is the older seller’s windfall. The younger buyer’s forty year mortgage is the older generation’s comfortable exit.

Then there is the national debt. It now costs over £100 billion a year just in interest payments. That money comes out of taxation every single year. It does not build hospitals. It does not fix roads. It does not fund schools. It is the annual charge for decades of spending more than was raised — spending that funded benefits and services that disproportionately went to older generations. The younger generation pays that bill in their taxes before a single penny is spent on anything they might actually use.

The result is a generation squeezed on every front they had no control over. Higher taxes to service a debt they did not run up. Inflated house prices in a market they had no hand in inflating. Forty year mortgages at a total cost that would have been unthinkable a generation ago. Stagnant wages that have gone nowhere in real terms since 2008 and provide no way out. Every one of these pressures was created by decisions made before they were old enough to vote. By a generation that is now telling them the arrangement is fair and that questioning it is out of order.

There is a financial product that makes this transfer impossible to ignore. It is called equity release. It allows older homeowners to unlock the value of their properties without selling them. The money gets spent — on retirement income, on holidays, on lifestyle. The debt sits against the property and gets paid back when the house is eventually sold.

Here is what that actually means. The value in those properties — the equity being unlocked — only exists because younger buyers are paying inflated prices. The older generation’s wealth is not abstract. It is real because younger people are taking on decades of debt to buy it. The equity release market is, in direct and measurable terms, funded by the mortgage payments of people forty years younger.

The younger generation is financing the retirement of the generation whose houses they are buying. Their debt is the collateral. Their inflated purchase price is the source of the wealth being spent. Their forty year repayment schedule is what makes the older generation’s equity real and spendable.

Nobody planned it this way. But the result is the same regardless. The younger generation is the financial engine underneath the older generation’s prosperity. And that engine is running on debt, flat wages, and a housing market deliberately kept expensive by the people now cashing out of it.

And here is the part nobody in British politics will say out loud. The pension system is not just struggling. It is mathematically broken. And the numbers that prove it are not complicated. Britain currently has around 33 million people in work and around 12 million pensioners. On the surface that looks like a ratio of roughly three workers for every pensioner. Tight but manageable.

But look closer. Of those 33 million workers, around 8.5 million are paid directly from taxation — the public sector, government funded bodies, and similar roles. They are counted as workers. But they do not contribute to the pot. Their wages come out of it. Strip them out and the real number of people generating the tax that pays for everything is closer to 24.5 million.

That gives a true ratio of around two net contributors for every pensioner. Not three. Two. And at two the system is already failing. We are already running massive deficits. We are already borrowing to cover the gap. We are already dependent on immigration to slow the rate of decline.

Now look forward to when a 20 year old today reaches retirement age. The pensioner population is projected to rise from around 12 million to somewhere between 18 and 20 million. The number of net contributors will not rise to match it. It will stay roughly where it is or fall. That collapses the ratio from two net contributors per pensioner to somewhere close to one.

One net contributor per pensioner. That is where this system is heading. And it was designed for three.

The arithmetic of that is brutal and unavoidable. To keep the pension system solvent on current tax and spending settings, with that collapsing ratio, the retirement age for a 20 year old today would need to rise to around 81. If life expectancy continues to increase, or if the contributor base shrinks further, that number moves into the mid-eighties.

Nobody is saying this. Nobody in Westminster is standing up and telling a 20 year old that the system as currently designed cannot give them what it gave their grandparents. That the promises made to the current pensioner generation were made on demographic assumptions that no longer exist and will never return. That the bill for those promises, on current settings, means working until you are over 80.

That is the reality. That is where the arithmetic leads. And the generation that designed this system, benefited from it, and protected it from every attempt at reform is the same generation now arguing that nothing should change.

A 20 year old in Britain today is not walking into a land of opportunity. They are walking into a country of accumulated debts, inflated prices, and a political system that has spent fifty years looking after everyone except them. So what will a 20 year old today inherit?.

They will pay more for housing relative to their wages than any generation in British history. They will pay the highest tax burden in seventy years, much of it going straight to service debt they did not create. They will fund a pension system built for a demographic balance that no longer exists and will never come back. They will retire later, on less, with less certainty, in a system that was not designed for them and has not been changed to help them.

And they will do all of this while being told by the generation that ran up the debt, inflated the assets, and wrote the pension promises that the current arrangement is fair, that reform is a betrayal, and that anyone who dares question the system is attacking vulnerable old people. The wealthiest retired generation in British history is telling the poorest-starting working generation in living memory that the arrangement is non-negotiable.

That is Britain in 2026.

Here is the question that cuts through everything. Two questions that destroy every remaining argument.

If pensioners genuinely believe the national debt has nothing to do with them — if they truly think that fifty years of accumulated borrowing is not their responsibility — then they have to answer this.

Who accumulated it?

It didn’t pile up while young people were running the country. It didn’t happen because 25 year olds were setting tax rates, writing budgets, winning elections, and deciding how much to spend. It accumulated across fifty years during which this generation was the dominant force in British politics. They were the biggest part of the electorate. They had the highest turnout. They were the most chased, the most courted, the most catered-to voting group in the country’s political history. Every government for fifty years built its spending, its borrowing, its tax policy, and its benefits around what this group wanted and what would keep them voting the right way.

The debt belongs to the decisions. The decisions belonged to the governments. The governments belonged to the electorate that kept returning them.

And then comes the second question. The one everyone already knows the answer to.

Who do they think should pay it?

The answer is not complicated. It has been given — not in words but in votes, in demands, in fifty years of resistance to any reform that might affect them.

The pensioners are saying “We accumulated it”, but “You youngsters have to pay it”.

That is not a political position. It is not an economic theory. It is not a principled argument about fairness or contribution. It is the most brazen passing of a bill in modern British history, dressed up in the language of entitlement and wrapped in a claim of victimhood that the numbers demolish completely.

The generation that ran British politics for fifty years is now refusing to own what those fifty years produced. The voting bloc that returned government after government committed to spending more than it raised, borrowing against the future, protecting house prices, and designing the pension system in its own favour — that group is now pointing at people who weren’t born, weren’t voting, and had no power to change any of it, and saying: you sort it out.

The 20 year old who had no vote in 1987. No voice in 1997. No power in 2003. No say in 2010. The 20 year old who inherited a housing market they cannot afford, a tax burden they did not create, a pension liability they did not design, and a national debt they had no part in building — that person is being handed the bill by the people who ran up the tab.

There is no version of that which is acceptable. There is no framing that makes it fair. There is no arithmetic that makes it sustainable.

The numbers have been making this argument for years. The debt is real. The deficit is real. The demographic pressure is real. The transfer of wealth from young to old is real. The squeeze on younger generations is real. The asset inflation that made one generation rich and priced the next one out is real. The wealth of today’s pensioners is real, measurable, and greater than any retired generation this country has ever seen.

What has been missing is the willingness to say it plainly.

Britain’s pensioners lived through the greatest expansion of wealth this country has ever seen. They voted, repeatedly and with massive effect, for the governments that built the system they now draw from. They were protected through every economic crisis of the last twenty years while everyone around them absorbed the pain. They are now demanding more — more money, more protection, more insulation from the reality that governs everyone else’s life.

Meanwhile the generation paying for all of that is being hit from every direction. They pay inflated prices for assets this generation inflated. They service debt this generation accumulated. They fund pension promises this generation made to itself. They do it on wages that have gone nowhere for twenty years in a housing market that was deliberately kept expensive by the political choices of the people now selling out of it.

This generation shaped Britain for fifty years. They had the votes and the power to change the direction at any point. They chose not to. They took the comfortable option every single time. And now the long-term cost has landed and they are looking the other way.

They are the richest retired generation in British history. They accumulated the debt. They elected the governments. They took the gains. They were protected through every crisis that hit everyone else.

And they have decided someone else should pay.

Accountability does not stop at retirement age. The numbers do not care how old you are. The debt does not disappear because you have stopped working. Fifty years of choices do not stop being your choices just because you are now elderly.

Britain’s pensioners do not get to walk away from what they built. The arithmetic will not allow it. The younger generation cannot afford it. And this country will not survive it if we keep pretending otherwise.

This conversation has been avoided for too long.

It needs to start now.